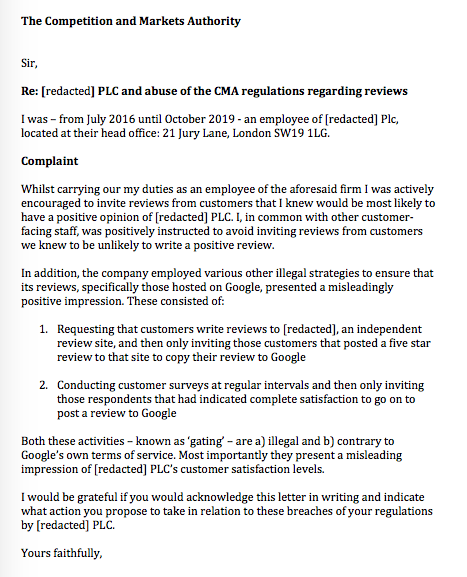

In 2020 you might expect some reference to researching using the net. But there is none. So we will pick up where this article left off.

The article references 'the damaging closure of high-profile Woodford Investment Management' so we will just add another three 'high-profile' names that have featured in the press recently to start a list of our own: St James's Place, Hargreaves Lansdown and Lindsell Train; we will then go on to examine the online presences of all the firms quoted in that article, after all, won't every investor looking for a new home for their portfolio be searching online as a first step - even if only to find contact details?

And right next to those contact details, in every single search?

Woodford

St James's Place (head office)

St James's Place (a typical office):

Hargreaves Lansdown

Linsell Train

Chase de Vere

Mattioli Woods

Brooks Macdonald

Quilter Cheviot

Barnett Waddingham

Brewin Dolphin

Last line of the article? 'It pays to do your homework'. All we can say is 'good luck' researching these businesses online, you'll get plenty on past performance (and we know what everyone, including the regulators, says about that) but next to nothing from their hundreds of thousands of existing clients about service levels. Even those that score well - see Brewin Dolphin above, where none of their three reviews appear to have been written by a 'real' client and Barnet Waddingham with a score of 4.9 from seven reviews, ditto (five being worthless ratings, four of which have been written by points-seeking local guides) have made no effort to harness the power of online reviews for the benefit of potential clients.

The article contained this survey:

We're going out on a limb here, but surely those who value 'personal attention' and 'quality and reputation' might also place a high value on a business that went to the trouble to invite and display customer opinions like this:

And this...

And this...

Surely the most cynical investment manager is going to acknowledge that at least some of their potential clients might be reassured by seeing that in excess of 100 of their existing clients were prepared to put 'pen to paper' to voice their approval of their service?

So why don't they?

We did the obvious thing. We asked some. They responded candidly (having been reassured their responses would be published anonymously). Here they are...

- "We expect the responses - and ratings - to correlate with clients' subjective experience of the performance of their portfolios."

- "We expect that our unhappy investors will be much more likely to post - therefore unfairly skewing our image."

- "Many of our clients are simply not financially savvy enough to make a reasoned judgment."

- "Our clients will object to being asked to publicly express an opinion of our services."

And, more than once...

- "None of our competitors have engaged with Google reviews."

We mined further down. Why not? The answer, when pressed, was invariably fear. Fear of the unknown, fear of losing control. So here's our answer to that 'fear'.

Fear that clients will focus on performance

Performance is one - important - aspect of any investment management service. But remember that clients do not need the business's permission to post a review on Google. One surefire way to ensure a negative online impression over the long term is to leave the field clear for unhappy clients. Remember that the business can always respond to the review, and use that response to educate their potential clients as well as address the contents of the individual review.

Fear that only those with an axe to grind will post reviews

This has been proven to be a 'false fear'; there is no evidence at all, across a range of high-value services where the business has proactively engaged. And that is the key: ignore consumers and the most disgruntle will post reviews, engage and happy loyal clients will way outnumber them.

Fear that clients don't understand financial services well enough to post an accurate review

This is where a service like HelpHound comes in. Our clients invariably invite their clients to write their review to them in the first place, this gives HelpHound the opportunity to moderate the review before publication. What is moderation? It is the act of checking a review for factual inaccuracies before it is published. Reviewers welcome it as much as our client businesses - after all, most reasonable people don't actively want to post an inaccurate or misleading review, they actually want to help their fellows make the right decision.

Fear that clients will resent being asked to write a publicly visible review

If anyone thinks that financial services are so sensitive as to be exempt from reviews then we would ask them to consider this client of ours, a Harley Street feminine health and wellbeing clinic.

There are perfectly reasonable grounds for this objection, after all, finance is a private matter. Our answer, based on extensive experience with similarly sensitive businesses, is that a - perhaps surprising - number of people are prepared, willing even, to share their experience for the benefit of their fellows. Remember that no one is forced to write a review, all that it takes is careful wording of the invitation (such experience we have in spades) making it quite clear to the recipient that their review is designed to help others and is entirely voluntary.

No other financial services business has engaged with reviews

We hope we have made a strong case for reviews in the context of investment management and financial services. We are confident that the first financial services businesses that engage will see immediate benefits, in much the same way that estate agents (hardly the most popular businesses!) have done - here is the monthly report Google sends every business (we recommend you seek out whoever in your business receives it, the data it contains is invaluable):

Aside from your business's Google score which anyone can easily find by simply googling your business, it contains vital information on...

- how many people found your business in Google searches in the previous month (2,653 in this client's case)

- how many calls you received directly through Google (73)

- how many visits to your website came as a direct result of finding you in a Google search (90)

...and, perhaps most important of all, any uplift in these numbers (important because the uplift, in this case, was as a direct result of joining HelpHound).

Further reading...

- Thousands could lose their life savings - why reviews matter (this article was written well before the Woodford storm broke, but would have been just as relevant in that context)

- Estate agents were - understandably - wary about adopting a proactive stance with reviews; see what five of them say here

- Unfair, fake, misleading or just plain inaccurate reviews do no-one any good, and they can seriously impact a business. Here's the happy ending for a case involving a client of ours.